Every market cycle there seems to be a financial foil. We’ve had the Dot.Com Delusion, the Housing Crisis Hydra and the Pandemic Pause. Today, the boogeyman is the AI Illusion and its deficits are printed both inside and outside the financial media. Is it a bubble? We don’t know. We’ll only know in hindsight.

But, let’s be honest - we can’t help ourselves. We click. We scroll. We consume headlines about bubbles, crashes and corrections like we’re scanning the savanna looking for the slightest movement.

For thousands of years, being jumpy kept us alive. Today, it just keeps us subscribed.

But risk is worth talking about - because most of what we fear isn’t actually risk at all. It’s noise.

Professional investors - think Warren Buffett and Howard Marks - define risk very simply: it is the chance of permanently losing your capital. Losing your money.

Not a bad month. Not a scary headline. Permanent loss.

And, that distinction matters.

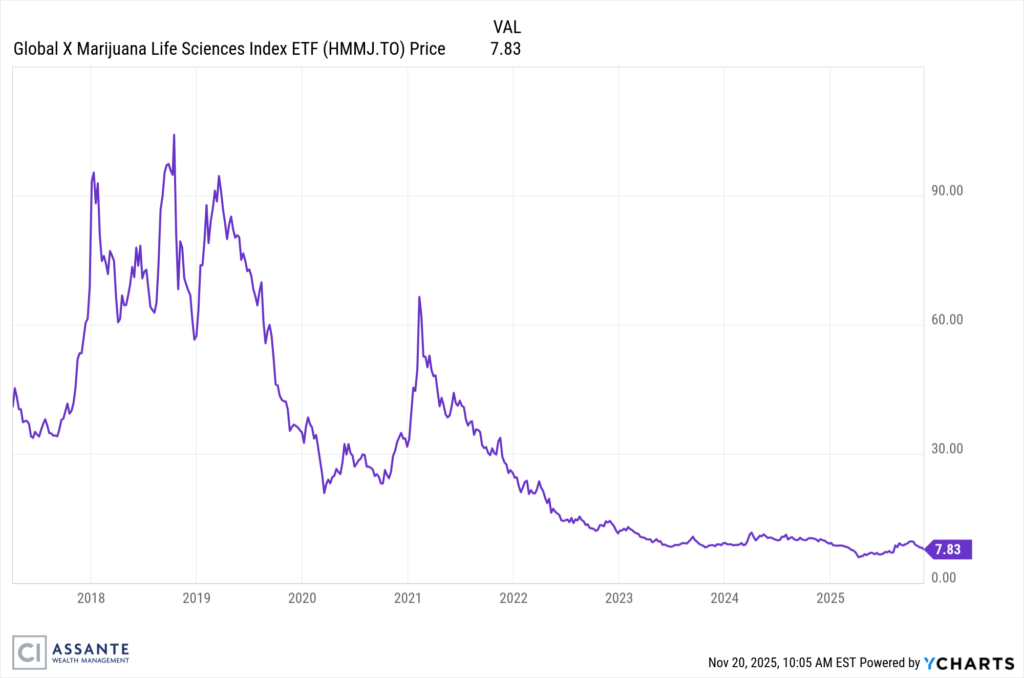

Example #1: Cannabis Stocks

Remember the pre and post cannabis legalization hype in 2019? Cannabis was going to supplant alcohol, cure diseases and give investors a rocket ride to wealth.

The Marijuana Life Sciences Index zoomed upward - then reality tapped the brakes - and never let go. Prices collapsed by 90% with many investors never recovering.

That’s not volatility. That’s a permanent loss of capital.

Example #2: Toronto Pre-Construction Speculation

Or consider the “assignment” craze in Toronto’s pre-construction condo market a few years ago. In many cases, buyers put down roughly $20,000 on an $800,000 unit with the expectation that they would sell the contract before closing.

Fast forward to today. The market has cooled, demand has softened and the developer is ready to close.

The challenge? The lender now appraises the condo at $650,000 - not the original $800,000.

That leaves a funding gap of roughly $150,000 that needs to be addressed quickly.

For some, that means dipping into registered savings or turning to family support - outcomes that can create lasting financial consequences.

That’s what we mean by permanent loss.

So, if this is risk… how do we measure it?

Enter: Volatility - The Imposter

The financial industry holds onto volatility as the marker for risk because, in my opinion, it gives us a nice, neat number - standard deviation – to easily label and sort investments into low, medium and high-risk buckets.

But volatility is not the risk Buffett or Marks is talking about. If the S&P500 goes down by 14% on average each year, does that mean it is risky when it does.

Worrying about that is like waking up shocked that it snowed in Ottawa in February. Yes, it’s annoying, but it’s entirely normal.

A Better Lens: Time Horizon & Outcomes

Portfolio swings are gut wrenching but if we stretch out the y-axis (i.e. time) we find that volatility washes away.

Using the S&P500 we observe that since 1928 you had a 75% chance of having a positive year, after 3 years an 85% chance of a positive experience, after 5 years 90% and after 10 years 95% with the average rate of return being 12%.

Imagine, someone said that you had a 75%, 85%, 90% or 95% chance of winning a blackjack hand how would you feel?

Time crushes volatility into irrelevance.

The $1M Portfolio Thought Experiment

Day 1: You invest $1,000,000.

Year 1: +15% → $1,150,000

Year 2: +10% → $1,265,000

Year 3: –5% → $1,200,000

Now the question: Have you gained or lost?

Your instincts shout, “Oh man, I’m down $65,000 this year! That’s a new car!”

Your intellect whispers, “Don’t forget, you’re still up $200,000 over three years.”

That tension - between instinct and intellect - is the mental tug of war that we all wrestle with when investing.

Always Try and Zoom Out

Let’s talk about today. We’ve had three positive calendar years in a row - 2023, 2024 and 2025.

We do know this: volatility is inevitable.

So, the 4 prescriptions for volatility are:

- Stay diversified - Still the number one rule of not getting blown up during a downturn.

- Know your downside - Understand how much your portfolio can drop in a normal pullback - and get comfortable with that reality before it happens.

- Keep your short-term cash needs covered - Major purchases plus 12–18 months of withdrawals should be safely set aside in cash.

- Trust the businesses you own - The management teams behind the world-class companies in your portfolio have repeatedly adapted, innovated and steered through every kind of economic weather. That’s why we own them.

I hope this finds you all well and if you have any questions feel free to reach out.

Bryan Deviney is a Senior Financial Advisor with CI Assante Wealth Management Ltd. The opinions expressed are those of the author and not necessarily those of CI Assante Wealth Management Ltd. Please contact him at 416.216.6500 or visit www.bryandeviney.com to discuss your particular circumstances prior to acting on the information above. CI Assante Wealth Management Ltd. is a Member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization.

The case study mentioned in this presentation is provided for illustrative purposes only and does not represent an actual client or an actual client’s experience, but rather is meant to provide an example of our process and methodology. The results portrayed is not representative of all of our clients’ experiences.